Key takeaways

- Financial education can create acquisition advantages before core banking needs emerge.

- A learning relationship can support retention across multiple life stages.

- Education data can reveal readiness without forcing immediate product conversion.

- Banks can partner with specialist learning platforms instead of building every layer internally.

GoHenry turns youth banking into a pipeline

On 12 June 2026, The Guardian reported that Barclays had agreed to acquire GoHenry’s UK business from Acorns. The deal is expected to complete in 2027. GoHenry will keep its brand.

The strategic signal is larger than the transaction. Barclays is not only buying a prepaid card product for children. It is buying a trusted relationship with families before the first adult current account, credit card, ISA, loan or mortgage is in scope.

The Barclays announcement describes GoHenry as a platform for children aged 6 to 18, with prepaid debit cards, parental controls, savings goals, money lessons and Junior ISAs. It also says GoHenry serves more than half a million UK children and has helped more than two million young people build money skills since 2012.

Financial education shouldn’t have a start or end date.

Education is moving into the acquisition layer

Bank customer education used to sit outside the core commercial system. It was a school visit, a PDF, a community programme or a CSR line in the annual report. That model is too weak for a market where acquisition is expensive and many financial products are hard to understand.

A modern financial education strategy can do a different job. It can create demand before the product moment. A child learns saving. A student learns budgeting. A first-jobber learns tax, credit scores and investing risk. A parent learns how to set allowances. Each lesson creates context, trust and intent.

For a Head of Growth, this changes the funnel. The financial literacy app is no longer just a support tool. It becomes a repeat engagement surface, an SEO asset, a referral mechanic and a product discovery layer. That is education-led growth in a regulated category where trust compounds slowly.

- Teach the problem before asking users to choose the product.

- Use learning milestones as activation events.

- Turn complex onboarding into short, testable steps.

- Create habit loops around real money decisions.

- Let readiness signals guide timing instead of pushing every user into the same offer.

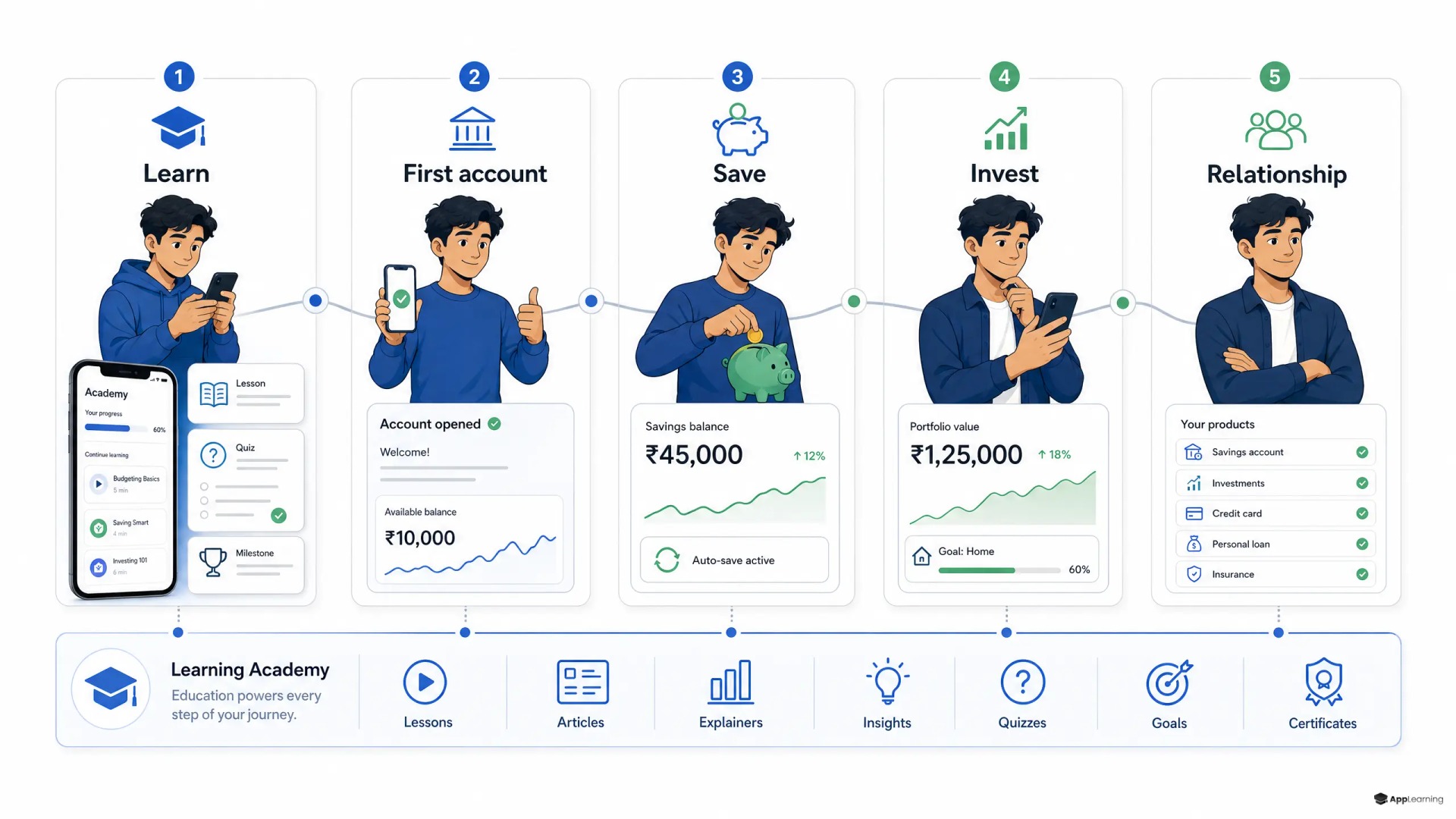

The lifecycle is the product map

Education works as distribution because financial needs arrive in stages. Pocket money becomes budgeting. Budgeting becomes income management. Income management becomes saving, investing, borrowing, insurance and long-term planning.

A bank or fintech that owns the learning layer can see where the user is in that journey. Not through invasive targeting, but through consented behaviour: completed modules, chosen goals, quiz results, skipped topics, repeated mistakes and declared plans.

That data is more useful than a cold audience segment. It shows readiness. A user who finishes three lessons on emergency funds is in a different state from a user browsing a high-yield savings account once. A user who completes a risk module before investing is better prepared than one who arrives from a paid ad.

This is where fintech customer acquisition can become more efficient. Paid media rents attention. Education earns it. Product teams can then connect lessons to onboarding, calculators, simulations, sandbox tools and product paths without making every interaction a sales pitch.

Good to know

How can financial education support fintech growth?

It creates a low-pressure entry point before users are ready to buy. That makes it useful for acquisition, activation and retention when the product requires trust or explanation.

When does education become disguised promotion?

It crosses the line when the lesson only exists to push one product. Good education teaches the decision, the risks and the alternatives before any conversion path appears.

Should banks build financial education platforms internally?

Some can, but many should partner. The bank brings trust, product knowledge and compliance oversight, while a learning platform brings instructional design, gamification and scalable content systems.

Trust breaks when lessons become ads

The main failure mode is disguised promotion. Users notice when education is just a product brochure with quizzes attached. Regulators notice too. The UK FCA says firms’ retail communications under Consumer Duty should support consumer understanding and be fair, clear and not misleading in its Consumer Duty handbook.

The operational rule is simple. A lesson must be useful even if the learner never buys the product. That does not make the system commercially weak. It makes the relationship durable.

- Separate curriculum objectives from product revenue targets.

- Teach costs, risks, alternatives and trade-offs before product benefits.

- Use age-appropriate content and parental controls where minors are involved.

- Measure comprehension and confidence, not only conversion.

- Offer product paths after learning milestones, not inside every lesson.

Build the learning layer before the next product push.

StartPartnership beats ownership for most teams

Barclays can acquire. Most banks and fintechs should not start there. The faster route is a partnership model that connects a branded academy to the product journey while keeping the learning experience credible.

This is where App-Learning fits naturally. The bank or fintech owns the strategy, compliance rules, brand and customer journey. A specialist learning partner builds the academy layer: curriculum design, gamified mechanics, content operations, analytics, certificates, nudges and AI-supported content workflows.

- A branded academy for top-of-funnel education and organic discovery.

- An onboarding academy that reduces drop-off in complex products.

- A lifecycle academy that moves users from basic knowledge to advanced needs.

- A partner academy for youth, family, employee or community financial education programmes.

The strategic question is no longer whether financial education belongs in banking. It already does. The real question is whether it is treated as a serious distribution system or left as disconnected content. Banks and fintechs that build the learning layer well will not just explain products better. They will meet customers earlier, understand them sooner and retain them longer.