Key takeaways

- Stablecoin UX must explain which protections users do and do not have.

- Payment education belongs at transaction moments, not only in help centers.

- Recourse literacy can reduce support load, complaint risk and user mistrust.

- Wallet education should cover finality, fees, redemption and escalation paths.

The rail is moving faster than the protection model

Stablecoin payment infrastructure is no longer a side topic for crypto teams. Major payment, banking, wallet, exchange and commerce firms are now building around dollar and sterling tokens. The promise is clear: faster settlement, broader reach, lower dependency on legacy correspondent paths, and more programmable money movement.

Regulators are moving as well. On 22 June 2026, the Bank of England published its policy statement and draft rules for systemic sterling stablecoin issuers, with the final Code of Practice intended by the end of 2026. That matters because payment products do not scale on infrastructure alone. They scale when users know what the system will do when something breaks.

Efficiency does not explain recourse

The stablecoin UX problem starts where most product decks end. Settlement speed is easy to explain. Recourse is harder. A card user often expects a dispute path, fraud handling, and a recognizable complaint process. In many stablecoin flows, the burden shifts toward the sender: check the network, check the address, understand gas, accept finality, and know which party can actually help.

A January 2026 systems paper on retail payment stablecoins argues that stablecoin arrangements often externalize fees, error prevention and dispute resolution to users, intermediaries and courts. That is not only a legal or compliance issue. It is a product education issue. If the user learns these differences after a failed transfer, the product has already lost trust.

externalize transaction fees, error prevention, and dispute resolution to users, intermediaries, and courts

The payment screen is the classroom

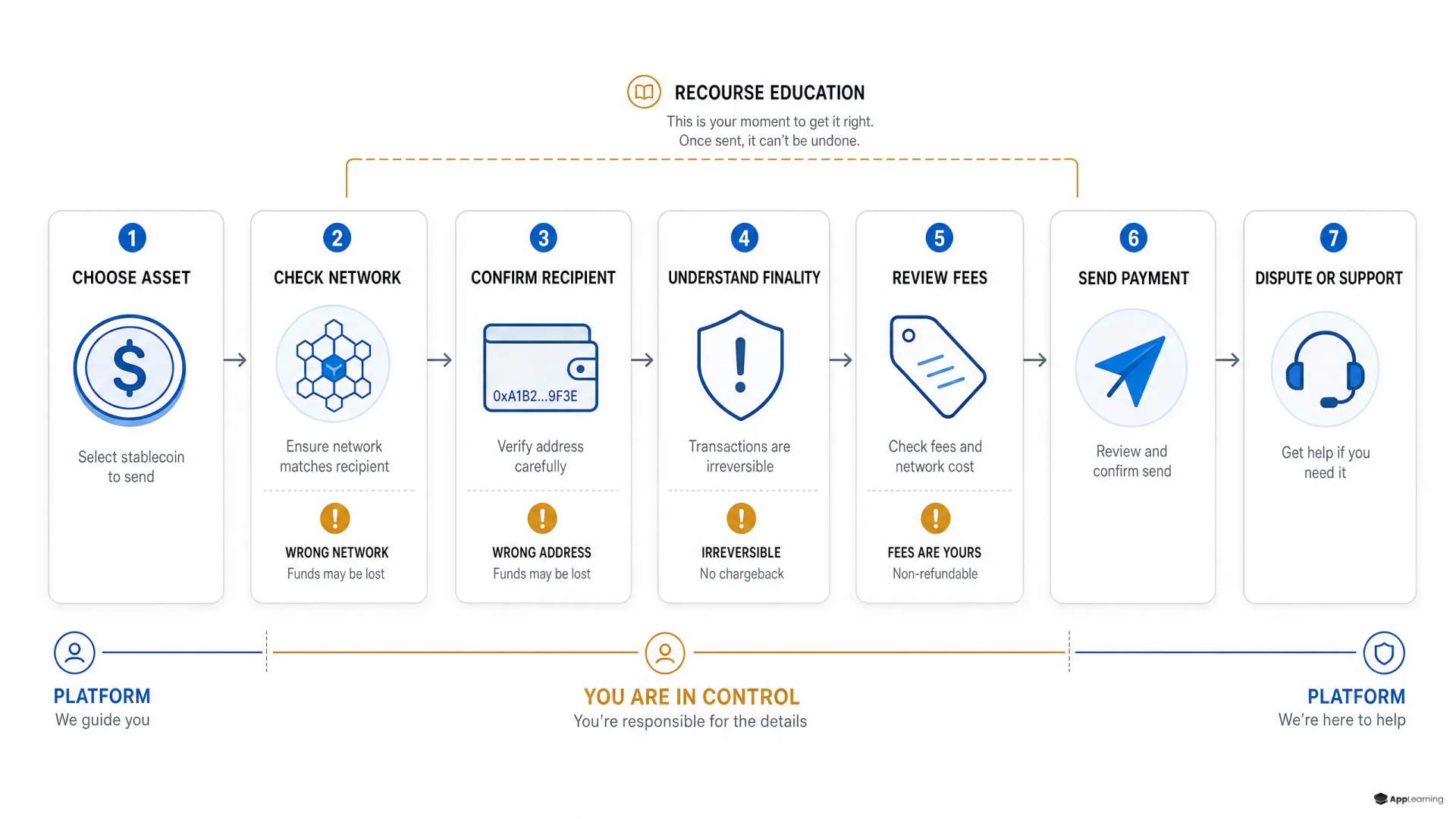

Good stablecoin payment education does not mean adding a long explainer before onboarding. It means placing small, clear interventions at the moments where misunderstanding creates loss. The payment screen, confirmation screen, pending state, failed transaction state, refund path and support escalation flow all carry different learning jobs.

- Before send: network, recipient, token, fees and finality.

- At confirmation: what can still be changed and what cannot.

- After send: status, settlement state, receipts and explorer links.

- On failure: who owns the next action and what evidence is needed.

- On refund or redemption: timing, fees, limits and counterparty role.

This is where crypto payment recourse has to become visible. Users do not need a blockchain lecture. They need to know whether a mistaken address can be reversed, whether a merchant can refund, whether a wallet provider can intervene, whether the issuer handles redemption, and when the only path is law enforcement or a formal complaint.

Good to know

Where should stablecoin payment education appear?

It should appear inside the payment journey, especially before confirmation, after submission, during failure states and inside support escalation flows.

What should users understand before sending stablecoins?

They should understand finality, network choice, fees, recipient checks, refund limits, redemption paths and which party can help if something goes wrong.

How can fintech teams measure whether wallet education works?

Track onboarding completion, first-transfer success, repeated support topics, quiz results, failed-payment recovery and drop-off around high-risk transaction steps.

Recourse literacy changes support economics

Traditional electronic payments have trained users to expect defined error-resolution paths. In the United States, for example, CFPB guidance on electronic fund transfers covers unauthorized transfers, debit card transactions, ACH, prepaid accounts and certain mobile payment transactions under Regulation E. Stablecoin products must be much more explicit when similar expectations do not apply, apply only partly, or depend on product structure.

The operational consequence is simple. If the interface does not teach recourse, support will. Agents will repeat the same explanations. Users will file confused complaints. Risk teams will push for heavier warnings. Product teams will see activation drop because the flow feels dangerous. Stablecoin customer onboarding should therefore measure understanding, not just completion.

Build payment education that users meet before mistakes happen.

Learn moreA practical education layer for wallet teams

For wallet, fintech and payment teams, the answer is not to slow the payment down. The answer is to design a thin education layer that adapts to risk. Low-value repeat transfers may need only a compact reminder. First-time transfers, new networks, new merchants, cross-border flows, redemption events and unusual fees should trigger stronger prompts.

- Use microcopy for simple transaction facts.

- Use short cards for unfamiliar concepts.

- Use quizzes for high-risk first actions.

- Use analytics to find repeated knowledge gaps.

- Localize examples for each market and language.

App-Learning can support this layer without turning the core product into a learning portal. The work is to map the user journey, identify moments of financial misunderstanding, build mobile-first microlearning, and connect quiz data to product analytics. That gives teams a way to improve wallet education while keeping engineering and product capacity focused on the payment system itself.

Stablecoins can reduce settlement friction. They cannot remove the user’s need for confidence. The next phase of stablecoin UX will be won by products that explain the consequences of payment before the user commits value. Speed gets the transaction started. Recourse education keeps the relationship intact when reality is less clean than the rail.