Key takeaways

- Stablecoins are becoming infrastructure, not only crypto assets.

- Infrastructure complexity creates education and trust gaps.

- Product education must explain money movement, custody, and redemption.

- Learning operations should keep pace with regulatory and technical changes.

The stablecoin story has moved beneath the interface

Stablecoins used to be taught as crypto primitives. That was enough when the lesson was the peg, volatility, and wallet setup. It is not enough when stablecoins move into payment orchestration, merchant settlement, payroll, treasury, and cross-border flows.

The shift is visible in the market structure. Reuters reported on January 14, 2026 that Visa was working to integrate stablecoins into existing payment systems. On June 30, 2026, Reuters reported that Open Standard brought together more than 140 businesses and announced Open USD, a U.S. dollar stablecoin expected to go live later in 2026. The product question is no longer whether users know what a stablecoin is. The question is whether they understand what must work behind the balance.

Businesses need something that’s open, low-cost, high-throughput, broadly accessible, and aligned to their interests.

Users need the map of money movement

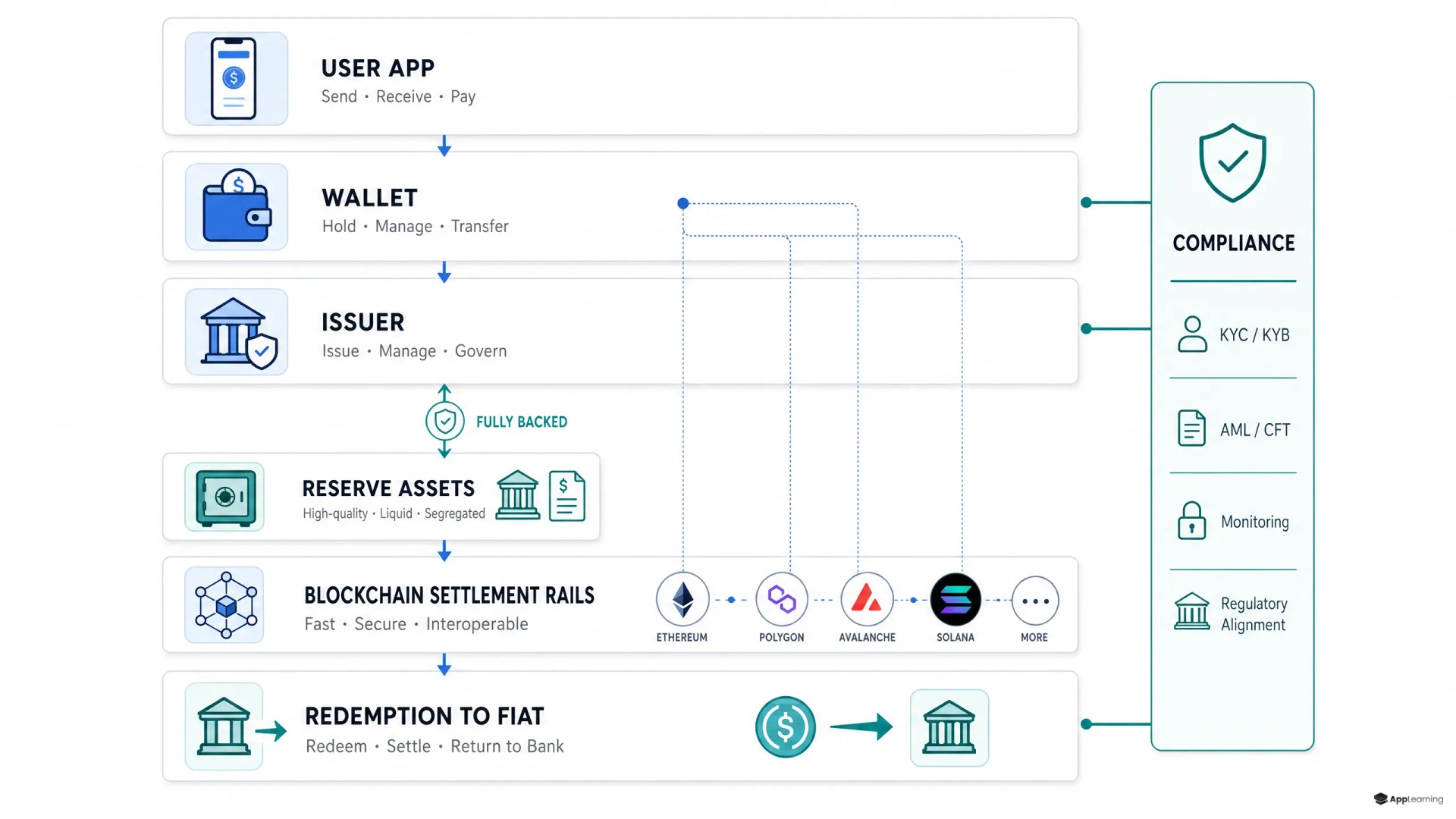

A balance in an app looks simple. The system behind it is not. A user may see dollars, euros, or a token ticker. The product team sees issuers, reserves, smart contracts, banking partners, custody models, compliance checks, chain selection, liquidity, and redemption paths.

Good digital money education makes those invisible dependencies legible without turning the product into a technical manual. It should explain who issues the token, what backs it, where the asset sits, how settlement happens, who controls the wallet, what happens during redemption, and what changes when value moves across chains or jurisdictions.

- Retail users need confidence that the balance can be used and redeemed.

- Business users need clarity on settlement timing, fees, limits, and reconciliation.

- Support teams need plain answers for repeated questions about failed transfers, pending transactions, and wallet access.

- Compliance teams need shared language for sanctions screening, transaction monitoring, custody, and disclosures.

- Product teams need analytics on which concepts block activation and feature adoption.

Shallow explainers create operational debt

A static page called What is a stablecoin will not carry a regulated payment product. It may answer the first question, but it leaves the operational questions open. Users then learn through tickets, abandoned onboarding, compliance friction, failed transactions, and social media speculation.

Regulators are also forcing the vocabulary to become more operational. In the U.S., the Treasury said the GENIUS Act tasks it with rules for payment stablecoins that address consumer protection, illicit finance risk, and financial stability risk. In Europe, the European Banking Authority describes MiCA requirements for asset-referenced tokens and e-money tokens, including issuer authorisation and technical standards. Education that ignores this layer will age fast.

The result is not only a trust problem. It is a product efficiency problem. Weak payment infrastructure education raises support load, slows onboarding, weakens adoption of high-value features, and makes internal teams repeat the same explanations in different formats.

A learning path for digital money plumbing

Stablecoin infrastructure education should be built as a journey, not as a glossary. The sequence matters because each concept depends on the last. Users cannot understand redemption risk if they do not understand the issuer. They cannot understand settlement status if they do not understand the rail.

- Start with the promise. What problem does the stablecoin feature solve inside this product?

- Explain the actor model. Issuer, wallet provider, custodian, exchange, bank, merchant, and user.

- Show the reserve model. What backs the token and what does redemption mean in practice?

- Map the transaction lifecycle. Funding, minting, transfer, screening, settlement, payout, and reconciliation.

- Make custody concrete. Self-custody, hosted wallets, recovery, permissions, and loss scenarios.

- Teach compliance as product behavior. Limits, checks, holds, rejected transfers, and documentation requests.

- Explain interoperability. Chains, bridges, token standards, network fees, and routing decisions.

- Close with exception handling. Pending payments, failed redemptions, chain congestion, account review, and support escalation.

This is where a fintech learning platform has to behave more like product infrastructure than content storage. It needs mobile-first modules, embedded checkpoints, version control, localisation, and analytics that show which knowledge gaps correlate with drop-off.

Good to know

Why is stablecoin education different from general crypto education?

Stablecoin education must explain money movement, reserves, redemption, custody, and compliance. General crypto education often stops at wallets, tokens, and market risk.

Who needs stablecoin infrastructure education inside a fintech product?

Retail users, business users, support teams, compliance teams, product teams, and partners all need different versions of the same operational map.

Should stablecoin learning sit inside onboarding or in a help center?

Both can help, but the most important lessons should sit inside the product flow where users make decisions, fund accounts, transfer value, or handle exceptions.

How should product teams measure whether the education works?

Track module completion, quiz results, activation rates, support topics, failed task recovery, feature adoption, and retention for users who completed the learning journey.

Learning operations must track the rail

Stablecoin products will change often. Partners will change. Supported chains will change. Redemption terms may change. Regulatory wording will change. A 2026 proposed U.S. federal rule discusses payment stablecoin issuers as financial institutions for Bank Secrecy Act purposes and refers to standards for issuance, purchase, redemption, custody, and transfer. That is not a one-time education problem. It is crypto learning operations.

For a product lead, the operating model should be clear. Every backend change that affects trust, access, cost, timing, custody, or compliance should trigger a learning review. Every support spike should feed the education backlog. Every onboarding cohort should show where users understand the rail and where they guess.

App-Learning fits this layer because the work is not only writing lessons. It is structuring modular education inside the product, keeping it aligned with fast-changing financial infrastructure, and using quizzes and learning analytics to reduce blind spots. The goal is not to make every user a blockchain expert. The goal is to make the product understandable enough that users act with confidence.

Build stablecoin education users can trust.

PlanConfidence is built in the backend story

Stablecoins will not win trust because the interface says instant, cheap, or digital. They will win trust when users understand the operating system behind those claims. Financial education must now explain the plumbing: issuer, reserve, settlement, wallet, custody, compliance, redemption, and interoperability. Products that teach this well will convert complexity into confidence. Products that avoid it will push the same complexity into support, risk, and churn.