Key takeaways

- Drop-off often signals uncertainty, not only excessive form length.

- Complex onboarding should sequence trust, comprehension, and action together.

- Embedded education works best at the exact point of hesitation.

- Activation metrics should track first value, confidence, and recovery from friction.

Complex products fail at moments of doubt

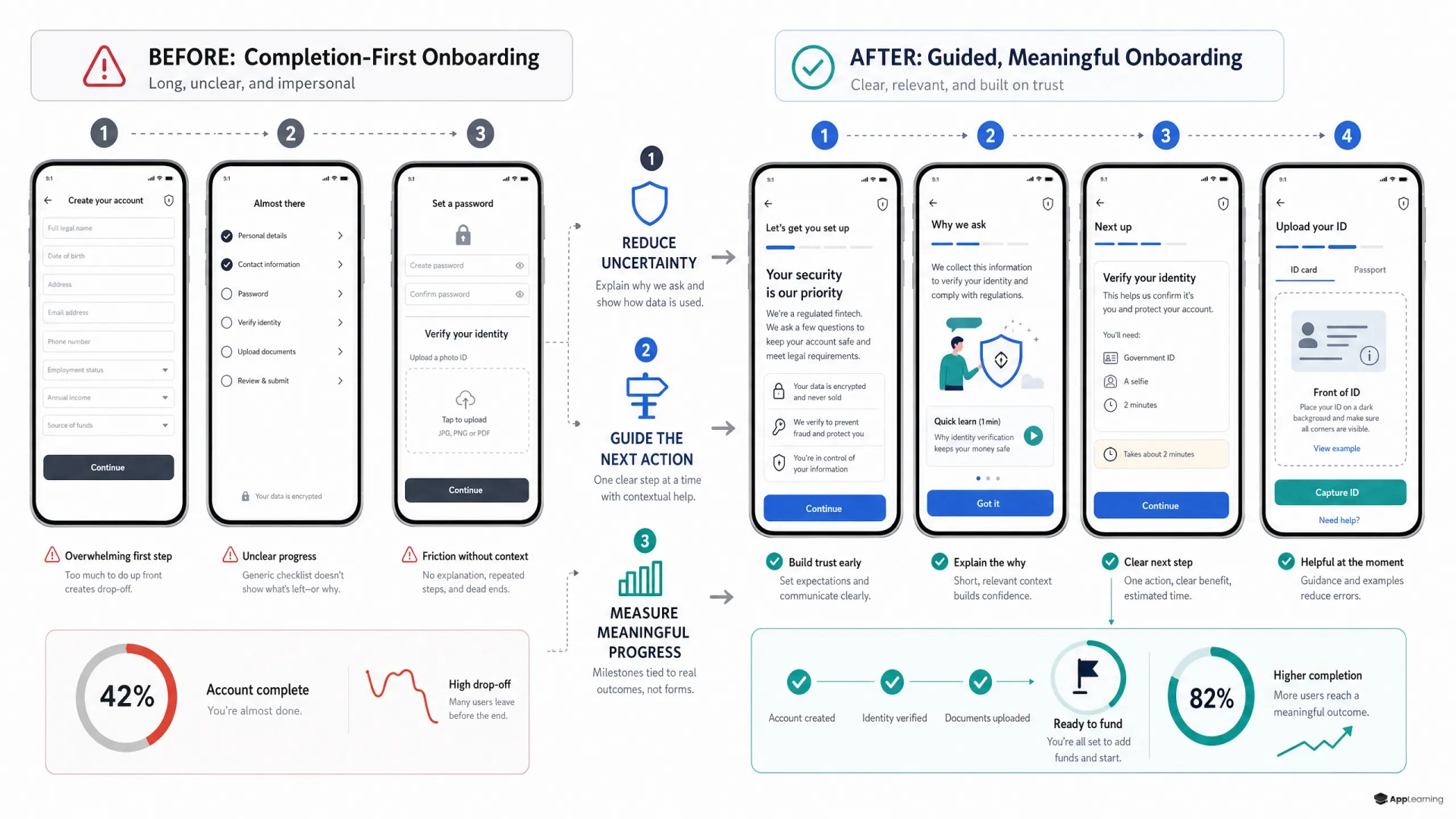

Many onboarding audits start with the same answer: make the flow shorter. Sometimes that helps. But in fintech, crypto, insurance, payments, and other regulated products, users do not only drop because a form has too many fields. They drop when the product asks for trust before the product has earned it. Connect this account. Upload this document. Accept this risk. Move this money. If the user cannot explain what happens next, the safest action is to stop.

Simple SaaS patterns do not travel well

Onboarding best practices from simple SaaS products often assume that the user can understand the product by doing one quick action. Complex products work differently. Value, risk, identity, eligibility, pricing, and compliance sit in the same journey. Regulation now reflects this reality: the FCA's Consumer Duty expects firms to give customers clear information at the right time and support informed decisions. That turns onboarding from a setup flow into a comprehension system.

The real drop off points are decision points

High-friction journeys tend to break at predictable points. The pattern is not random. Users hesitate when a step changes the level of commitment, exposes personal data, creates financial consequence, or introduces a term they do not understand. NIST's digital identity guidelines describe identity proofing as a process where resolution, validation, and verification each create distinct user challenges, which is a useful model for fintech onboarding more broadly.

- Identity verification and document upload

- Bank connection and data permissioning

- Funding, transfer, staking, or first trade

- Risk warnings and product eligibility checks

- Pricing, fees, lockups, limits, and reversibility

Good onboarding turns uncertainty into the next action

The best flows do not explain everything at once. They explain the next decision well enough for the user to continue with confidence. That means sequencing the journey around user questions, not internal systems. A KYC vendor, CRM field, risk disclosure, and lifecycle email may all be owned by different teams. The user experiences one journey. If the handoffs are not designed, uncertainty accumulates.

- Explain why sensitive data is needed before asking for it.

- Show the current step, the next step, and the expected time.

- Use examples when a term affects money, risk, or access.

- Give safe previews before irreversible or high-stakes actions.

- Create recovery paths for failed verification, missing documents, and abandoned funding.

Good to know

Which onboarding best practices matter most for fintech products?

Focus on decision points. Explain sensitive data requests, financial consequences, risk terms, and the next action before the user has to decide.

Should complex onboarding always be shorter?

No. Remove unnecessary steps, but do not remove the context users need to trust the product and act with confidence.

What is a better activation metric than setup completion?

Track the user's first meaningful value action, then measure how quickly and confidently users reach it after registration.

Progress metrics beat setup metrics

A completed account is not the same as an activated user. A user can finish KYC, skip funding, ignore risk education, and never reach the product's value. The metric problem is common: teams measure what systems can see, not what the user has understood. Better onboarding metrics connect setup completion with first-value behavior and the support cost of confusion.

- Time to first meaningful action

- Completion of the first value path, not only registration

- Drop-off by decision point and product concept

- Recovery rate after failed KYC or stalled funding

- Support tickets caused by unclear steps or terms

- D7 and D30 retention by education exposure

Education belongs inside the journey

A help center is useful for motivated users. It is weak at the moment of hesitation because the user must leave the flow, search, interpret, and return. Embedded education works differently. It appears where the question forms. The FCA's 2025 cryptoasset consumer research reported very high public awareness of cryptoassets, but awareness does not equal readiness to act safely. Good onboarding closes that gap with short, contextual explanations, checks for understanding, and guided practice before commitment.

Map onboarding to first value.

Map itThe operating model shifts from content to capability

This is where App-Learning fits best. The task is not to publish more educational content around the product. The task is to make education part of the product system. Product, growth, compliance, lifecycle, and CX need shared maps of the concepts users must understand, the moments where those concepts matter, and the metrics that show whether learning changed behavior. In complex fintech products, onboarding improves when teams stop treating education as support material and start treating it as activation infrastructure.

The strongest onboarding is not the shortest journey. It is the clearest path from uncertainty to competent action. Users need to know what is being asked, why it matters, what risk they are accepting, and what successful progress looks like. When that system is designed well, drop-off becomes easier to diagnose, trust becomes easier to build, and first value becomes easier to reach.