Key takeaways

- Prioritize journeys and audiences before producing more content.

- Use modular formats so education can scale with the product.

- Tie learning assets to activation, adoption, trust, and retention goals.

- Measure behavior change, not only course completion.

- Embed education where product decisions actually happen.

Customer education usually starts with good intent. A product manager writes a help article after a confusing release. Customer success records a demo after ten similar support calls. Marketing runs a webinar when a new feature needs attention. None of this is wrong. The problem is that these assets rarely form a customer education strategy.

This becomes painful in fintech. The product may depend on terms, risk models, compliance steps, payment flows, identity checks, custody choices, tax concepts, or market mechanics that users do not already understand. If education sits outside the journey, users must leave the product to make sense of it. Many will not come back.

For regulated financial products, education is not only a growth lever. It is also part of trust. Under the FCA Consumer Duty guidance, firms should give customers the information they need at the right time, in a way they can understand, and with regard to their level of financial literacy.

Firms should support their customers by giving them the information they need, at the right time.

Fragmentation starts with good intent

Fragmented customer education is not a content problem at first. It is an ownership problem. Product explains features. Growth explains value. Support explains errors. Compliance reviews claims. Customer success explains workflows. Each team optimizes its own surface, so the user gets a pile of disconnected explanations.

The symptoms are easy to recognize. The onboarding checklist links to long articles. The help center is accurate but hard to navigate. Webinars repeat basic questions. New features ship with product tours but no real learning path. Support keeps answering questions that should have been prevented earlier.

As the product grows, the maintenance burden grows faster than the content library. Every pricing change, compliance update, new market, or UX change creates hidden debt. If there is no modular system, teams must update the same explanation in five places. That is how customer education becomes expensive without becoming strategic.

Strategy starts with journeys not assets

A scalable customer education strategy begins with the user journey. The first question is not what content should we create. The first question is where understanding blocks progress.

For a fintech or crypto product, the highest-value education moments are often not the most obvious topics. The user may not need a full course on stablecoins. They may need a 90-second explanation at the exact moment they choose a network, approve a transfer, compare yield, activate a card, or connect an account.

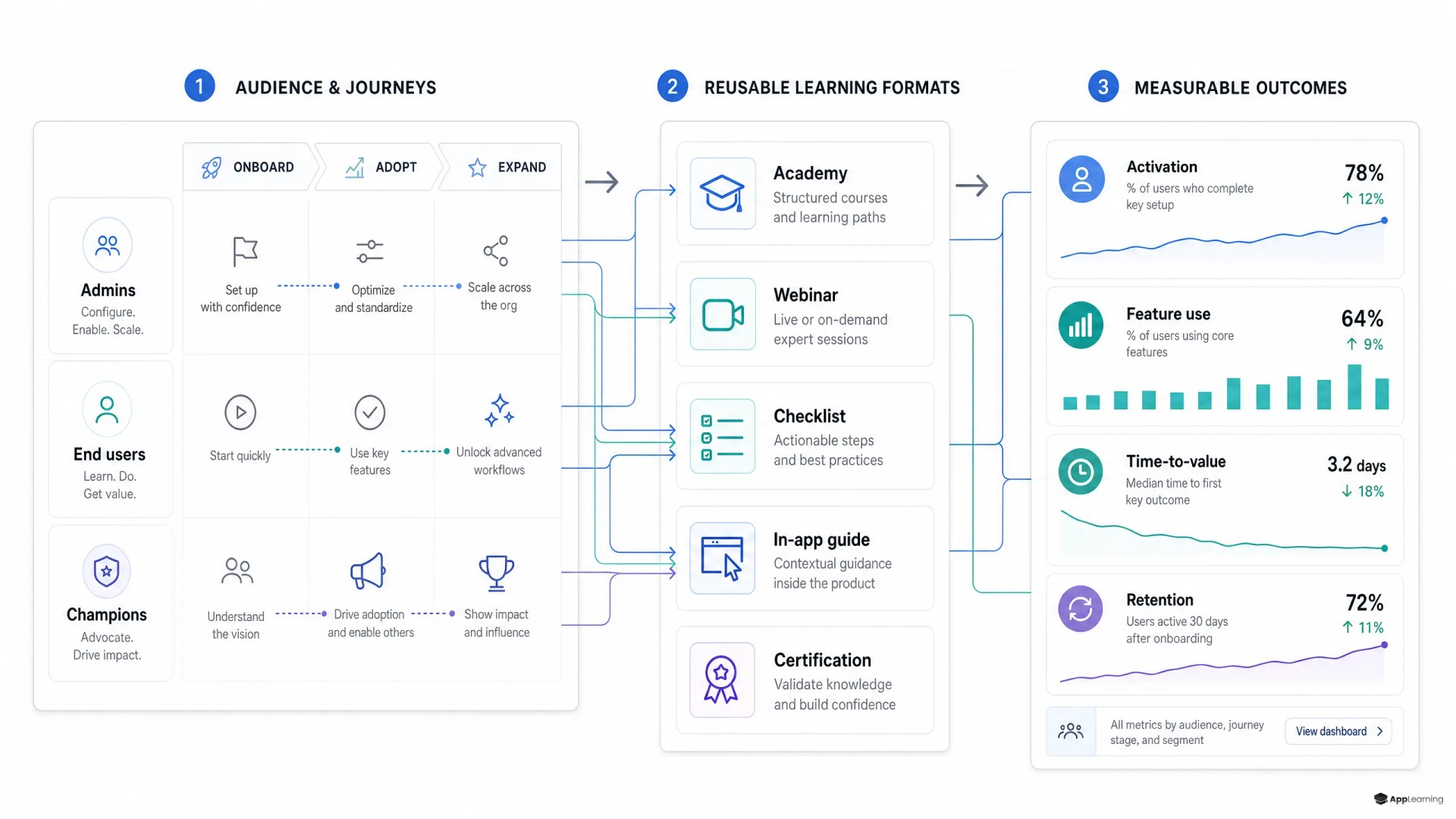

- Audience first. Separate new users, activated users, power users, partners, and internal teams.

- Journey stage second. Map education to signup, verification, first transaction, feature adoption, expansion, and reactivation.

- Learning outcome third. Define what the user must understand, decide, or do after the learning moment.

- Format last. Choose the smallest format that can create the required behavior change.

This order matters. Teams that start with format usually overproduce. They launch courses where a product-embedded card would work better. They record webinars where a short diagnostic quiz would reveal the real gap. They publish articles that are correct but disconnected from the moment of decision.

The moments that deserve education

Not every feature needs a lesson. Scalable customer education focuses on moments where misunderstanding creates measurable business cost. In fintech, those moments tend to cluster around activation, trust, and correct usage.

- Activation moments, where the user must complete setup before they feel value.

- Risk moments, where the user must understand fees, volatility, fraud, limits, or irreversible actions.

- Feature discovery moments, where the user has a goal but does not know the product can help.

- Habit moments, where the product needs repeated use to become valuable.

- Recovery moments, where an error, declined transaction, failed verification, or support contact can either destroy trust or rebuild it.

This is where product and growth teams should work from the same map. The activation funnel shows where users drop. Support tags show what users misunderstand. Product analytics show which features are ignored. Compliance reviews show where language needs more care. Together, these signals identify where education can change behavior.

Large crypto and fintech brands already treat education as a product surface. Coinbase describes Coinbase Learn and Learning Rewards, Binance operates Binance Academy, and Revolut documents Crypto Learn as an in-app education tool. The lesson is not to copy their libraries. The lesson is to treat learning as part of the customer experience.

Reusable formats beat one-off production

One-off assets do not scale because each asset has its own structure, review path, analytics gap, and maintenance cycle. A better system uses repeatable formats that can be reused across topics and journeys.

For complex financial products, the strongest formats are usually modular. A five-minute lesson explains one concept. A quiz checks one decision rule. A glossary clarifies one term at the point of need. A scenario shows one real use case. A certificate can mark readiness for a higher-risk workflow or partner requirement.

- Concept cards for terms users must understand before acting.

- Scenario lessons for risk, fraud, compliance, and product fit.

- Interactive quizzes for confidence checks and segmentation.

- Learning paths for onboarding, advanced adoption, and partner enablement.

- Contextual deep links from product screens to specific lessons.

- Dashboards that show completion, drop-off, quiz accuracy, and user progress.

This is the operating logic behind scalable customer education. The education team does not rebuild from scratch every time the product changes. It updates modules, swaps examples, localizes lessons, and connects the right learning object to the right journey moment.

In the Invity Academy case, App-Learning helped turn static Bitcoin education into an embedded academy inside the app, with short lessons, quizzes, certificates, bilingual content, and contextual product calls to action. The important pattern is not the visual format alone. It is the connection between learning, product context, and user confidence.

Good to know

Where should a fintech team start with customer education?

Start with the journey stage where misunderstanding creates the biggest drop-off or support burden. For many fintech teams, that is onboarding, identity verification, first transaction, or first use of a high-value feature.

How much content is needed for a first customer education program?

Less than most teams expect. A strong first version can be a small set of modular lessons, quizzes, and glossary items tied to one activation or adoption goal.

Who should own the customer education strategy?

Ownership can sit in Product, Growth, Customer Success, or Education, but the system must be cross-functional. Product should define the journey, Growth should measure behavior, Compliance should review sensitive claims, and Content should maintain clarity.

What makes customer education scalable?

Scalability comes from reusable formats, clear governance, modular updates, segmentation, embedded delivery, and analytics. It does not come from publishing more isolated articles.

Measurement turns education into an operating system

If customer education is meant to support activation, adoption, and retention, it must be measured against those outcomes. Completion is useful, but it is not enough. A user can finish a lesson and still fail to activate. A user can watch a webinar and still never adopt the feature.

Measurement should run on two levels. Learning metrics show whether the education experience works. Business metrics show whether it changes customer behavior.

- Learning metrics include starts, completions, drop-off points, quiz accuracy, repeated attempts, time to finish, and certificate rates.

- Activation metrics include KYC completion, first deposit, first transaction, connected account setup, card activation, or first successful workflow.

- Adoption metrics include feature usage, breadth of product usage, repeat usage, and advanced workflow completion.

- Trust metrics include support contacts, complaint themes, risk warnings understood, fraud-reporting behavior, and confidence signals.

- Retention metrics include educated versus uneducated cohort retention, churn, reactivation, and expansion.

A 2025 LearnUpon survey reported that 35% of organizations saw difficulty measuring impact or ROI as one of their biggest customer education challenges, while only 25% had adopted dedicated customer education platforms. That gap explains why many teams believe education matters but struggle to prove it through operating data, as shown in LearnUpon customer education research.

The practical fix is cohort measurement. Compare users who reached a relevant learning milestone with similar users who did not. Then look at the next product behavior. Did they finish onboarding faster. Did they use the feature more often. Did they contact support less. Did they stay active longer. This does not make education the only cause, but it creates a disciplined way to learn what works.

The platform decision is a governance decision

A customer education platform is not just a place to host content. It decides how education is governed. It shapes who can update lessons, how reviews happen, how users are segmented, how learning connects to product surfaces, and how impact is reported.

For fintech teams, this matters because educational content often touches product, legal, compliance, support, and marketing at once. If updates require engineering work every time, education will lag behind the product. If analytics live outside the growth stack, impact will stay anecdotal. If learning is not embedded into onboarding and lifecycle flows, users will treat it as optional reading.

The App-Learning platform is built around branded academies, short lessons, gamified quizzes, learning paths, progress analytics, and fast course production. Its product material also describes deep links, embeds, single sign-on, role-based tracks, and dashboards for completions, drop-off points, popular courses, time spent, and exportable reports. Those capabilities matter because scalable education needs both learner engagement and operational control.

The same pattern appears in internal capability building. In the Bitsonauts Academy case, Bitso moved from repeated expert workshops to a consistent academy for crypto literacy across teams and countries. For customer education, the operating principle is similar. Replace repeated explanation with a reusable system that keeps improving.

Build a customer education system your users can finish.

TalkCoherence is the real advantage

A scalable customer education strategy does not mean more content. It means less waste, clearer ownership, better timing, reusable formats, and measurement that links learning to product outcomes. The strongest systems teach users before confusion becomes churn. They put education inside the journey, not beside it. They make complex products feel usable without hiding the complexity that users need to understand.

For fintech and crypto companies, that coherence is a growth asset. Users do not stay because a company has a large academy. They stay because they understand what to do, why it matters, what risks exist, and how to get value with confidence. Customer education becomes strategic when it stops being a library and starts becoming part of the product system.